Recommended Blogs

Test Automation for Core Banking Systems Drives Faster Releases

Table of Content

- Why Core Banking QA Has Become a Strategic Risk Lever

- What Test Automation for Core Banking Systems Actually Changes

- Where Manual QA Breaks Down in Core Banking Modernization

- Comparing Core Banking Modernization QA Approaches

- Automated Regression Testing BFSI: What to Prioritize First

- Decision Framework: When to Use Selenium, API Automation, or Model-Based Testing

- How Can TestingXperts Assist with Test Automation for Core Banking Systems?

- Conclusion

Share On

Core banking changes fail quietly before they fail publicly. A missed regression, delayed batch issue, or broken API contract can turn a routine release into an operational incident.

That is why test automation for core banking systems now belongs in executive technology conversations. McKinsey reported that global banking technology spending grew 9 percent yearly and reached $650 billion in 2023, yet many banks still struggle to prove release value.

The real question is no longer whether QA can test faster. The question is whether QA can maintain trust as banking teams release more frequently.

Why Core Banking QA Has Become a Strategic Risk Lever

Core banking QA sits at the heart of revenue, compliance, and customer confidence. It validates the systems that process deposits, loans, payments, interest, fees, and balances.

A delayed release may irritate product teams. A defective release can affect account accuracy, regulatory reporting, customer access, and operational continuity.

The Risk Profile Has Changed

Modern banking releases rarely affect a single application in isolation. A pricing change may affect mobile banking, middleware, account servicing, reporting, and downstream ledgers.

That complexity makes traditional QA governance too slow and too narrow. Test teams need evidence across business rules, integrations, data flows, and operational controls.

For CIOs and CTOs, QA has become a risk intelligence function. It shows whether the bank can change safely without slowing delivery beyond market tolerance.

Strong QA also enables leaders to have better release conversations. Teams can discuss residual risk, not just defect counts and test completion percentages.

What Test Automation for Core Banking Systems Actually Changes

Test automation for core banking systems changes QA from repeated manual checking into repeatable assurance. It gives teams faster feedback on high-risk workflows after every meaningful code change.

Automation does not remove banking complexity. It makes that complexity visible, measurable, and easier to govern across release cycles.

What Automation Should Cover

Core banking automation should focus on business-critical flows before peripheral screens. Mature programs usually cover these areas first.

- Account opening, servicing, closure, and customer profile updates

- Deposits, withdrawals, transfers, payments, and standing instructions

- Loan origination, repayment schedules, fees, and interest calculations

- Batch processing, reconciliation, general ledger postings, and reports

- APIs connecting digital channels, middleware, partners, and payment rails

This is where financial software test coverage becomes strategically useful. Leaders can see which revenue and risk areas are protected by automation.

Banking QA automation services also help standardize coverage across teams. That matters when modernization programs involve vendors, internal engineering, and legacy platform specialists.

IBM describes banking automation as handling repetitive, rules-based processes, which fit many regression scenarios. QA leaders should still maintain exploratory, risk-based testing for judgment-intensive cases.

Where Manual QA Breaks Down in Core Banking Modernization

Manual QA struggles as release frequency increases while banking complexity remains unchanged. Teams can add testers, but they cannot scale human attention indefinitely.

The pressure becomes visible during regression cycles. Testers repeat familiar checks while new defects hide in integrations, data transformations, and business-rule combinations.

Common Failure Points

Manual-heavy QA usually breaks in predictable places during core modernization. The symptoms appear operational before they appear strategic.

- Regression cycles consume most available testing capacity

- Test data becomes stale, inconsistent, or difficult to refresh

- API and UI tests duplicate effort without shared traceability

- Defect leakage rises when business rules change late

- Release teams accept risk without reliable coverage evidence

Legacy platforms make this harder because documentation often lags reality. Experienced testers possess critical system knowledge that scripts and test cases cannot capture.

That creates a serious risk of continuity. When key people move roles, institutional memory disappears with them.

CI/CD banking testing requires automated checks that run early and often. Manual QA remains valuable, but it cannot provide release of confidence on its own.

Comparing Core Banking Modernization QA Approaches

Core banking modernization does not follow one universal testing model. The right QA approach depends on platform age, release appetite, architecture, and risk tolerance.

Some banks still run large manual regression cycles before quarterly releases. Others build automation into delivery pipelines and use manual testing for complex judgments.

Four Practical Models

- Manual regression remains useful for unstable requirements and early discovery. It becomes expensive when teams repeat the same checks every release.

- Selective automation targets stable, high-volume workflows first. This model works when budgets are limited, and leadership needs measurable progress.

- Platform-led automation builds reusable frameworks across channels, APIs, and core services. It suits banks with multi-year modernization programs and shared architecture standards.

- Continuous testing embeds automation into CI/CD banking testing pipelines. This model works best when engineering teams own quality alongside QA.

No model eliminates tradeoffs. Heavy UI automation may mimic user journeys, but it often costs more to maintain. API-first automation gives faster feedback, yet it may miss presentation-layer defects.

Leaders should compare approaches by business risk, not tool preference. The best model protects critical banking outcomes with the least maintenance burden.

Automated Regression Testing BFSI: What to Prioritize First

Automated regression testing of BFSI programs often fails when teams automate everything equally. Core banking QA needs to be prioritized based on transaction value, defect history, and operational exposure.

The first candidates should be stable, frequent, and financially material. These tests generate reliable returns because teams run them repeatedly across releases.

High-value Regression Priorities

Start with workflows that directly affect money movement and customer trust. These areas usually justify automation before lower-risk administrative scenarios.

- Customer onboarding and KYC-linked account creation

- Funds transfers, bill payments, standing instructions, and reversals

- Interest accrual, fee charging, tax handling, and balance updates

- Loan repayment schedules, delinquency rules, and closure events

- End-of-day batch jobs, reconciliation, and exception reporting

Test data strategy matters as much as scripting. Banking tests need realistic account states, balances, limits, products, and customer types.

A weak data model creates false confidence. The automation may pass, while production-like combinations remain untested.

QA teams should also tag tests by business capability and risk tier. Executives then see coverage in language that matches banking priorities.

That reporting shift matters. It turns automation from a technical activity into a release governance asset.

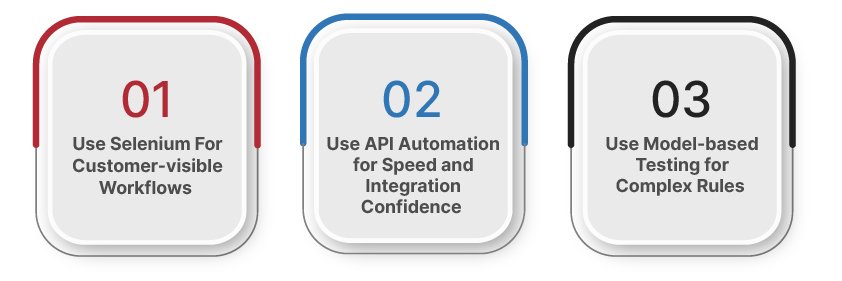

Decision Framework: When to Use Selenium, API Automation, or Model-Based Testing

Tool selection should follow system behavior, not team habit. Selenium banking automation, API testing, and model-based testing solve different QA problems.

The wrong choice creates fragile suites that teams eventually stop trusting. The right choice improves confidence without inflating maintenance costs.

Use Selenium For Customer-visible Workflows

Selenium works well for browser-based banking workflows with stable interfaces. It validates user journeys across login, navigation, form handling, and transaction confirmation.

Use it for critical digital banking paths where visual behavior matters. Avoid relying on Selenium for every business rule below the interface.

Use API Automation for Speed and Integration Confidence

API automation works best when services expose transaction logic clearly. It validates integrations faster than UI tests and supports frequent pipeline execution.

This approach suits payment services, account services, eligibility checks, pricing APIs, and partner integrations. It also supports more robust negative testing for limits, errors, and authentication.

Use Model-based Testing for Complex Rules

Model-based testing is helpful when business rules generate many valid path combinations. Lending, fees, interest, and product eligibility often fit this pattern.

The method requires upfront modeling discipline. It pays off when manual case design cannot reliably cover enough scenarios.

A balanced suite usually combines all three. API tests provide breadth, UI tests protect key journeys, and models expose rule combinations.

How Can TestingXperts Assist with Test Automation for Core Banking Systems?

TestingXperts helps banks move from fragmented automation to governed quality engineering. The focus is practical coverage, maintainable frameworks, and faster release confidence.

For test automation for core banking systems, TestingXperts supports automation strategy, tool evaluation, framework design, script development, and maintenance. Its Automation Testing Services reference Tx-Automate, a tool-agnostic framework supporting web, mobile, API, on-prem, and cloud applications.

The framework integrates with tools such as Selenium, Playwright, Cypress, JIRA, Azure DevOps, Jenkins, SauceLabs, and LambdaTest. That tool coverage helps banks align automation with existing delivery ecosystems.

TestingXperts also brings the BFSI context through digital banking and core banking experience. Its banking QA leadership content identifies specialist experience across core banking transformation, payments, and financial services delivery.

The engagement model can support automation-readiness assessment, regression-suite optimization, CI/CD banking testing enablement, and automation CoE setup. This gives IT leaders a structured path from tactical scripts to enterprise QA governance.

Conclusion

Faster banking releases do not come from testing less. They come from testing the right risks earlier, faster, and more consistently.

Test automation for core banking systems provides leaders with stronger evidence before production decisions. It also helps QA teams maintain trust as modernization programs continue to move forward.

Banks that treat automation as assurance infrastructure will release with more confidence. Those who treat it as scripting will keep fighting the same regression backlog.

VP, Delivery Quality Engineering

Manjeet Kumar, Vice President at TestingXperts, is a results-driven leader with 19 years of experience in Quality Engineering. Prior to TestingXperts, Manjeet worked with leading brands like HCL Technologies and BirlaSoft. He ensures clients receive best-in-class QA services by optimizing testing strategies, enhancing efficiency, and driving innovation. His passion for building high-performing teams and delivering value-driven solutions empowers businesses to achieve excellence in the evolving digital landscape.

Discover more