According to a recent study, more than 70% of Canadians now use digital banking services, and this number is expected to continue to grow. With this increase in usage comes an increased need for security and accessibility. Banks in Canada must meet regulatory standards for data privacy, user experience, and accessibility, among other standards.

To ensure that they are meeting these standards, Canadian banks are turning to Quality Assurance(QA) testing. Digital banking QA services are an essential part of the development process, allowing banks to identify and address any issues before they become major problems. By conducting regular QA testing, banks can ensure that their digital banking services meet regulatory requirements, providing Canadians with a secure and accessible banking experience.

In this blog, we will explore the regulatory requirements for digital banking in Canada, the role of QA testing in meeting these requirements, and how Canadian banks are implementing effective QA testing processes to ensure compliance and provide a positive user experience.

Why is it Important to Comply with Digital Banking?

Compliance with regulatory requirements is crucial for digital banks in Canada for several reasons:

Consumer Protection:

Digital banking involves the handling of sensitive personal and financial information, and this information must be protected. By ensuring compliance with regulations, banks can assure their customers that their data is secure and their online banking experience is safe.

Reputation Management:

Banks that are seen as non-compliant with regulatory requirements can quickly lose the trust of their customers, which can have a negative impact on their reputation. Maintaining compliance helps Canadian banks to maintain a positive reputation and attract more customers.

Financial Stability:

Compliance with regulatory requirements helps to ensure that digital banks are operating safely and stably, which is beneficial for the financial system as a whole. By avoiding costly mistakes, such as data breaches, banks can maintain stability and reduce the risk of financial losses.

Legal Obligations:

Canadian banks have a legal obligation to comply with regulatory requirements, and failure to do so can result in significant fines and other penalties. Ensuring compliance helps Canadian banks to avoid legal problems and protect their bottom line.

Future Growth

By maintaining compliance with regulatory requirements, Canadian banks can position themselves for future growth. Customers are more likely to trust banks that are seen as responsible and compliant, which can help banks to expand their customer base and grow their business.

Compliance with regulatory requirements is critical for the success of digital banks in Canada. By ensuring that their digital banking services are secure, accessible, and user-friendly, Canadian banks can meet the needs of their customers and position themselves for long-term success.

Purpose Of Study

The purpose of the study of digital banking compliance in Canada is to better understand how Canadian banks are meeting the regulatory requirements set forth by the Canadian government. This study aims to:

• Assess the current state of digital banking in Canada and the extent to which banks are complying with regulatory requirements.

• Evaluate the role of Quality Assurance(QA) testing in ensuring compliance and maintaining a positive user experience in digital banking.

• Identify best practices in digital banking compliance and the challenges faced by banks in meeting regulatory requirements.

• Provide insights into the future of digital banking in Canada, including trends and challenges, and how banks can prepare for the changing landscape.

Regulatory Requirements for Digital Banking in Canada

In Canada, the regulatory requirements for digital banking are set forth by various government agencies, including the Office of the Superintendent of Financial Institutions (OSFI) and the Canadian Bankers Association (CBA). These requirements are designed to ensure that digital banking services are secure, accessible, and user-friendly, and that customer information is protected.

Some of the key regulatory requirements for digital banking in Canada include:

Data Security:

Banks are required to implement robust security measures to protect customer information, such as encryption, firewalls, and multi-factor authentication.

User Authentication:

Banks must implement measures to verify the identity of customers accessing digital banking services, such as strong passwords and biometric authentication.

Risk Management:

Banks must implement risk management processes to minimize the risk of fraud and other security-related issues.

Banks must keep detailed records of all digital banking transactions and activities to ensure that customer information is protected.

Reporting:

Banks must report any security-related incidents, such as data breaches, to the relevant authorities promptly.

In addition to these requirements, Canadian banks must also comply with various other regulations, including Anti-Money Laundering (AML) laws and the Personal Information Protection and Electronic Documents Act (PIPEDA). By ensuring compliance with these regulations, Canadian banks can provide safe and secure digital banking services to their customers, while also promoting financial stability and protecting customer information.

Overview of Relevant Legislation and Regulations

In Canada, digital banking is regulated by several legislation and regulations, including:

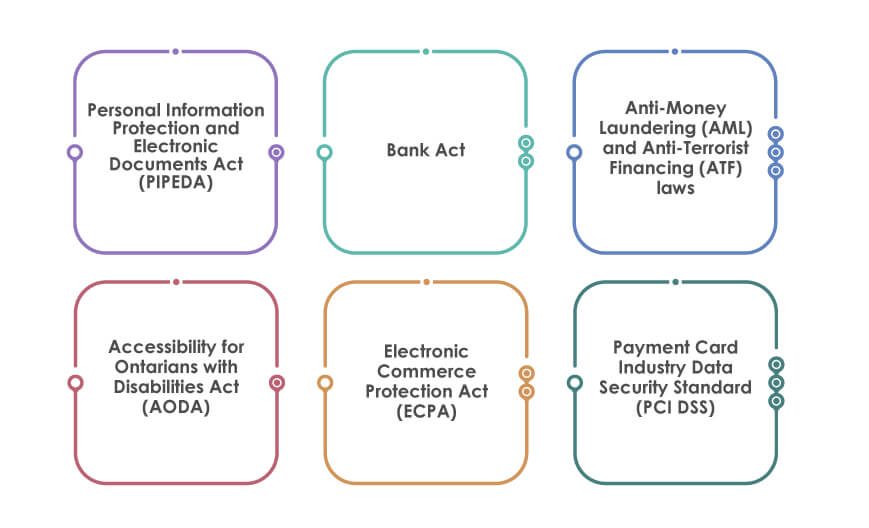

Personal Information Protection and Electronic Documents Act (PIPEDA):

This act sets the privacy rules for the collection, use, and disclosure of personal information in the course of commercial activities.

Bank Act:

This act sets out the framework for the regulation of banks in Canada and establishes the powers and responsibilities of the Office of the Superintendent of Financial Institutions (OSFI).

Anti-Money Laundering (AML) and Anti-Terrorist Financing (ATF) laws:

These laws require banks to implement measures to detect and prevent money laundering and terrorism financing activities.

Accessibility for Ontarians with Disabilities Act (AODA):

This act sets out the accessibility standards for the public sector, including the provision of accessible digital banking services.

Electronic Commerce Protection Act (ECPA):

This act sets out the criminal law relating to the unauthorized use of computer systems, unauthorized access to data, and unauthorized interception of data.

Payment Card Industry Data Security Standard (PCI DSS):

This is an international security standard set by the Payment Card Industry Security Standards Council (PCI SSC) to ensure that all companies that accept, process, store, or transmit credit card information maintain a secure environment.

These regulations are designed to protect customers and their information, promote financial stability and ensure that digital banking services are secure, accessible, and user-friendly. By complying with these regulations, Canadian banks can provide high-quality digital banking services to their customers, while also reducing the risk of security-related issues and protecting their reputation.

Standards for Accessibility and user Experience

In Canada, the standards for accessibility and user experience in digital banking are set by various organizations, including the Office of the Superintendent of Financial Institutions (OSFI), the Canadian Bankers Association (CBA), and the Accessibility for Ontarians with Disabilities Act (AODA). These standards aim to ensure that digital banking services are accessible to all customers, regardless of ability and provide a positive user experience.

Some of the key standards for accessibility and user experience in digital banking in Canada include:

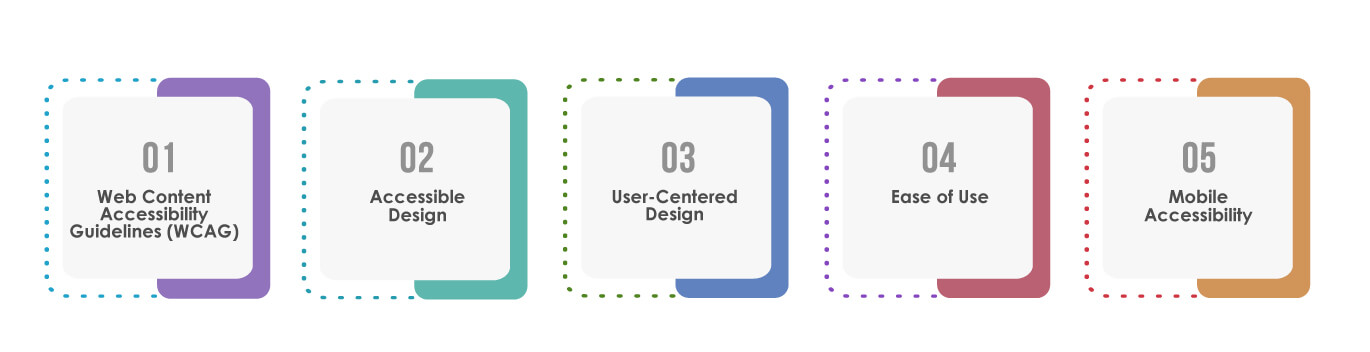

Web Content Accessibility Guidelines (WCAG):

These guidelines set out the standards for making web content accessible to people with disabilities, including the use of alternative text, clear headings, and consistent navigation.

Accessible Design:

Banks must ensure that their digital banking services are designed to be accessible to all customers, including those with disabilities, through the use of accessible design principles, such as large text and high-contrast colors.

User-Centered Design:

Banks must focus on the needs and preferences of customers when designing digital banking services, through the use of user-centered design methods, such as user testing and surveys.

Ease of Use:

Banks must ensure that their digital banking services are easy to use and understand, through the use of simple language and intuitive navigation.

Mobile Accessibility:

Banks must ensure that their digital banking services are accessible on mobile devices, including smartphones and tablets, through the use of responsive design and mobile-friendly interfaces.

By adhering to these standards, Canadian banks can ensure that their digital banking services are accessible and user-friendly, providing a positive experience for all customers. This not only meets regulatory requirements but also enhances customer satisfaction and loyalty, contributing to the overall success of digital banking in Canada.

Requirements for Data Privacy and Security

In Canada, digital banking is subject to some regulations and legislation related to data privacy and security. These requirements aim to protect the personal and financial information of customers and ensure the confidentiality, integrity, and availability of this data.

Some of the key requirements for data privacy and security in digital banking in Canada include:

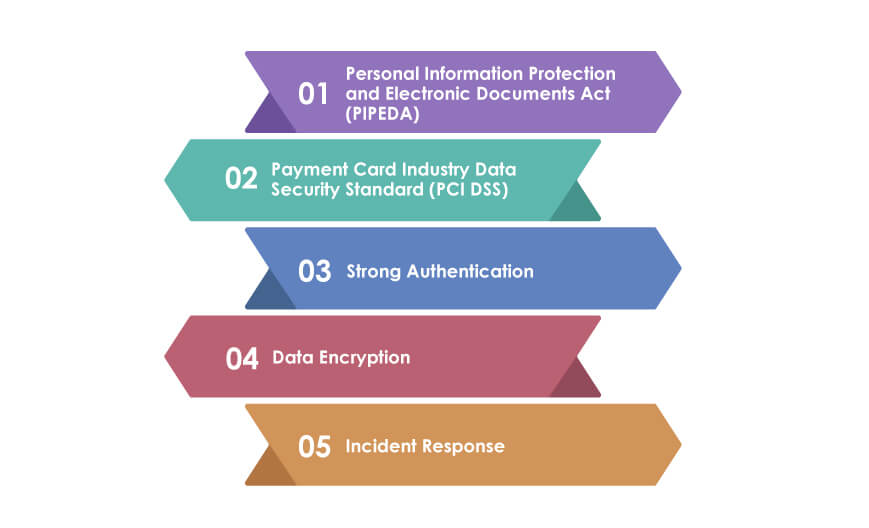

Personal Information Protection and Electronic Documents Act (PIPEDA):

This act establishes the rules for the collection, use, and disclosure of personal information in the private sector, including digital banking. Banks must comply with PIPEDA by ensuring that customer data is collected, used, and disclosed in a manner that is consistent with the act.

Payment Card Industry Data Security Standard (PCI DSS):

Banks that process credit and debit card transactions must comply with the PCI DSS, which sets out the standards for protecting cardholder data. This includes the use of encryption, firewalls, and access controls to secure cardholder data.

Strong Authentication:

Banks must ensure that customers can securely access their accounts through the use of strong authentication methods, such as multi-factor authentication or biometrics.

Data Encryption:

Banks must ensure that customer data is encrypted both in transit and at rest, through the use of encryption technologies such as SSL/TLS or AES.

Incident Response:

Banks must have a plan in place for responding to data breaches and other security incidents, including the reporting of incidents to relevant authorities and the notification of affected customers.

By adhering to these requirements, Canadian banks can ensure that customer data is protected and secure, reducing the risk of data breaches and protecting the reputation and trust of their customers. This also helps to maintain the stability and security of the financial system, contributing to the overall success of digital banking in Canada.

The Role of QA Testing in Meeting Regulatory Requirements

Quality Assurance (QA) testing plays a critical role in helping Canadian banks meet the digital banking regulatory compliance requirements for digital banking. QA testing is the process of evaluating the functionality, performance, and security of a digital banking system to ensure that it meets the specified requirements and standards.

Through QA testing, banks can identify and resolve any potential issues or vulnerabilities in their digital banking systems before they become a problem. This helps to ensure that the system is secure, reliable, and user-friendly and that it complies with all relevant regulations and standards.

Some of the key areas where QA testing can help banks meet regulatory requirements include:

Accessibility:

QA testing can help to ensure that digital banking systems are accessible to all users, regardless of their abilities or disabilities. This includes testing for compliance with accessibility standards such as WCAG 2.1 and ensuring that the system is usable by individuals with a range of abilities and disabilities.

Data Privacy and Security:

QA testing can help to identify and resolve any potential security vulnerabilities in digital banking systems. This includes testing for compliance with data privacy and security regulations such as PIPEDA and PCI DSS and ensuring that customer data is protected at all times.

User Experience:

QA testing can help to ensure that digital banking systems provide a positive user experience for customers. This includes testing for functionality, performance, and ease of use, and ensuring that the system is intuitive and user-friendly.

Compliance:

QA testing can help banks to demonstrate their compliance with all relevant regulations and standards. This includes testing for compliance with accessibility standards, data privacy, and security regulations, and any other relevant legislation.

By conducting thorough QA testing, Canadian banks can ensure that their digital banking systems meet regulatory requirements and provide a high-quality user experience for customers. This helps to maintain the stability and security of the financial system and supports the overall success of digital banking in Canada.

Conclusion

Canadian banks are making significant strides in meeting regulatory requirements in digital banking. They are investing in technology and cybersecurity measures to ensure the safety of their customers’ personal and financial information. The implementation of stronger authentication processes, such as biometric verification, has increased the level of security for online banking transactions. Additionally, the adoption of open banking initiatives, such as the introduction of APIs, has facilitated the integration of third-party financial services and improved the overall customer experience. The results of these efforts are reflected in the statistics, with a reported increase of 12% in digital banking usage in Canada in the past year. As the trend toward digital banking continues to grow, Canadian banks are committed to staying ahead of the curve and providing their customers with secure and convenient banking options.

How can TestingXperts help Canadian Banks Meet Regulatory Requirements in Digital Banking?

TestingXperts is committed to helping Canadian banks meet regulatory requirements in digital banking and provide high-quality, secure, and reliable digital banking services to their customers. By leveraging its expertise in software testing and quality assurance, TestingXperts is playing a key role in ensuring the success of Canadian digital banking.

TestingXperts Differentiators

We can play a crucial role in helping Canadian banks meet regulatory requirements in digital banking. Here are some ways in which a testing organization can assist:

Develop comprehensive testing plans:

Work with Canadian banks to develop a comprehensive testing plan that includes all aspects of digital banking, including mobile and online platforms, data security, and fraud prevention.

Conduct thorough testing:

Execute rigorous testing to ensure that the bank’s digital banking systems are functioning as expected and meeting regulatory requirements. This include both manual and automated testing of various scenarios to identify potential issues and ensure that the system meets the necessary standards.

Provide feedback and recommendations:

Provide feedback and recommendations to the bank on areas that require improvement or adjustment to meet regulatory requirements. This can help the bank to address any issues and improve their systems and processes to ensure compliance.

Keep up-to-date with regulatory changes:

Stay up-to-date with regulatory changes and requirements to ensure that the bank’s digital banking systems remain compliant. They can provide regular updates to the bank on any changes and help to ensure that the bank is prepared to meet new regulations.

Maintain documentation:

Detailed documentation of all testing activities and results, which can be useful in demonstrating compliance to regulatory bodies. This documentation can also be used to identify areas of improvement and track progress over time.